What Does Mortgage Investment Corporation Do?

The Mortgage Investment Corporation Diaries

Table of ContentsEverything about Mortgage Investment CorporationThe Mortgage Investment Corporation DiariesThe 6-Second Trick For Mortgage Investment Corporation

This suggests that capitalists can take pleasure in a stable stream of money flow without needing to actively handle their investment portfolio or fret about market changes. Furthermore, as long as consumers pay their mortgage on time, earnings from MIC investments will continue to be steady. At the same time, when a borrower ceases making payments promptly, investors can depend on the experienced team at the MIC to deal with that scenario and see the loan via the departure procedure, whatever that looks like.

Appropriately, the goal is for capitalists to be able to access stable, lasting money moves generated by a large capital base. Rewards received by shareholders of a MIC are generally categorized as passion revenue for objectives of the ITA. Capital gains realized by a capitalist on the shares of a MIC are normally subject to the normal treatment of capital gains under the ITA (i.e., in the majority of situations, taxed at one-half the rate of tax obligation on common earnings).

While certain requirements are unwinded up until shortly after completion of the MIC's very first fiscal year-end, the adhering to requirements need to normally be pleased for a company to receive and keep its standing as, a MIC: homeowner in Canada for objectives of the ITA and included under the legislations of Canada or a province (special policies put on companies incorporated before June 18, 1971); only task is spending of funds of the company and it does not handle or establish any real or immovable residential or commercial property; none of the residential or commercial property of the firm includes debts owning to the firm safeguarded on genuine or immovable building found outside Canada, financial obligations owning to the firm by non-resident individuals, except financial debts protected on real or immovable property positioned in Canada, shares of the funding stock of firms not homeowner in Canada, or actual or immovable property positioned outside Canada, or any kind of leasehold rate of interest in such residential or commercial property; there are 20 or more shareholders of the company and no shareholder of the firm (together with particular persons connected to the investor) has, straight or indirectly, more than 25% of the released shares of any course of the capital stock of the MIC (particular "look-through" guidelines use in respect of depends on and collaborations); holders of favored shares have a right, after repayment of preferred returns and payment of rewards in a like amount per share to the owners of the usual shares, to individual pari passu with the holders of typical shares in any kind of further returns payments; at least 50% of the price amount of all residential or commercial property of the firm is spent in: debts protected by home mortgages, hypotecs or in any other manner on "homes" (as specified in the National Real Estate Act) or on residential or commercial property included within a "real estate task" (as specified in the National Housing Serve as it kept reading June 16, 1999); down payments in the records of many Canadian link banks or lending institution; and money; the cost amount to the company of all genuine or unmovable property, including leasehold rate of interests in such residential property (excluding certain amounts acquired by foreclosure or pursuant to a debtor default) does not surpass 25% of the price amount of all its residential property; and it abides with the responsibility limits under the ITA.

The Single Strategy To Use For Mortgage Investment Corporation

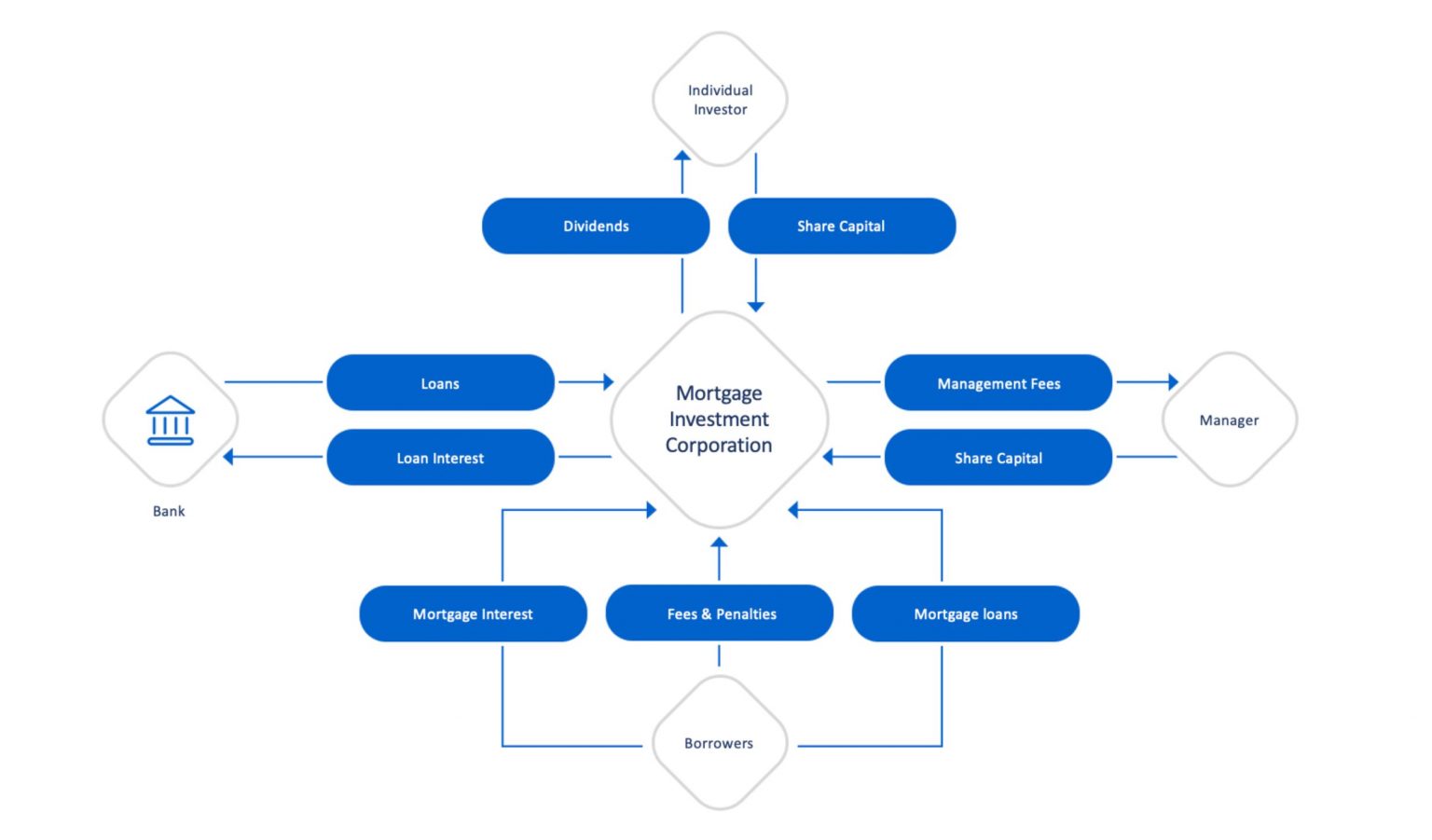

Resources Framework Private MICs commonly released 2 courses of shares, typical and preferred. Common shares are usually provided to MIC founders, directors and officers. Usual Shares have ballot legal rights, are normally not qualified to returns and have no redemption feature yet get involved in the circulation of MIC possessions after directory preferred shareholders obtain built up however unsettled dividends.

Preferred shares do not commonly have ballot legal rights, are redeemable at the option of the owner, and in some circumstances, by the MIC. On winding up or liquidation of the MIC, favored investors are usually entitled to obtain the redemption value of each preferred share along with any type of declared More Help yet unsettled rewards.

One of the most commonly depended on program exceptions for private MICs distributing securities are the "recognized investor" exemption (the ""), the "offering memorandum" exception (the "") and to a minimal level, the "household, buddies and business partners" exemption (the "") (Mortgage Investment Corporation). Capitalists under the AI Exemption are commonly higher total assets financiers than those who might only satisfy the limit to invest under the OM Exception (depending on the territory in Canada) and are likely to spend higher amounts of resources

4 Easy Facts About Mortgage Investment Corporation Shown

Capitalists under the OM Exemption usually have a reduced total assets than accredited investors and depending upon the territory in Canada go through caps valuing the quantity of capital they can invest. In Ontario under the OM Exception an "qualified investor" is able to invest up to $30,000, or $100,000 if such capitalist gets viability guidance from a registrant, whereas a "non-eligible financier" can only invest up to $10,000.

Historically low rate of interest in the last few years that has led Canadian investors to increasingly venture into the globe of exclusive home loan investment companies or MICs. These structures assure constant returns at a lot greater yields than conventional fixed revenue financial investments nowadays. However are they too good to be real? Dustin Van Der Hout and James Rate of Richardson GMP in Toronto assume so.